Income Tax Return (ITR) is a form which a person is supposed to submit to the Income Tax Department. It contains information about the person’s income and the taxes to be paid on it during a particular financial year, i.e. starting on 1st April and ending on 31st March of the next year.

ITR filing in India is a process where individuals and entities report their income, deductions, and taxes to the Income Tax Department. It is mandatory for individuals and businesses whose income exceeds the specified threshold to file their ITR. Here is an overview of ITR filing in India:

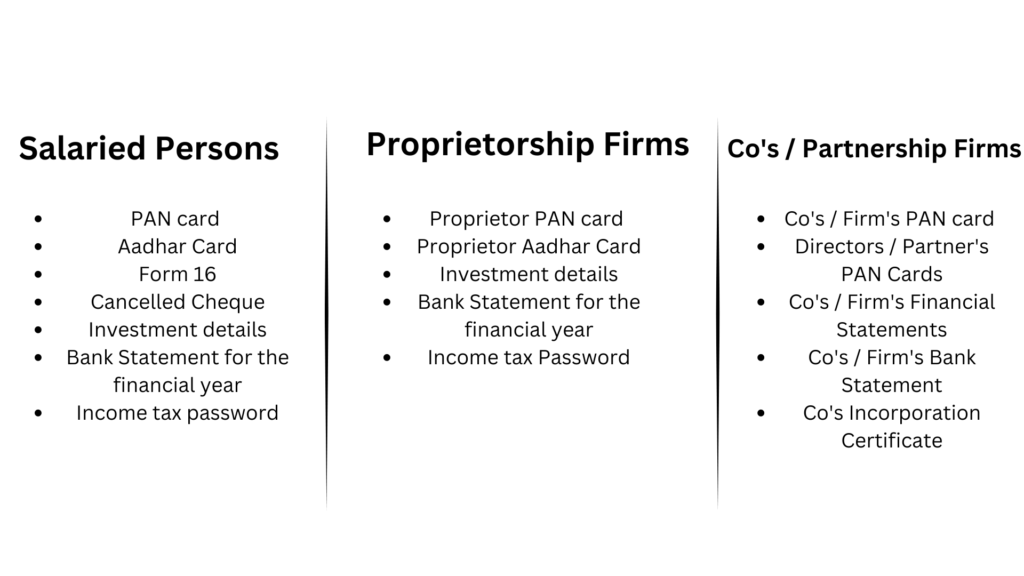

Eligibility: Individuals, Hindu Undivided Families (HUFs), companies, partnerships, and other entities are required to file ITR if their income surpasses the prescribed threshold.

Types of ITR Forms: The Income Tax Department provides various types of ITR forms to cater to different taxpayer categories and income sources. These forms are numbered as ITR-1, ITR-2, ITR-3, etc., and each form has specific eligibility criteria.

Income Sources and Deductions: Taxpayers need to disclose their income from various sources such as salary, house property, capital gains, business/profession, and other income. They can also claim deductions under different sections of the Income Tax Act to reduce their taxable income.

Filing Methods: ITR can be filed online through the Income Tax Department’s e-filing portal or offline by submitting a physical copy at the designated income tax office. Online filing is more convenient and popular, offering different methods like e-filing with a digital signature or e-verification using Aadhaar OTP or net banking.

Deadline: The deadline for filing ITR in India is usually July 31st of the assessment year (AY) for most taxpayers. However, the due date may vary based on the taxpayer category and specific circumstances. It is advisable to file the ITR within the specified timeline to avoid penalties and interest.

Importance and Benefits: Filing the ITR is not only a legal obligation but also carries several benefits. It serves as proof of income, facilitates loan and visa processing, supports claims for deductions and refunds, and maintains financial records for future references.

Compliance and Penalties: Non-compliance with ITR filing requirements can result in penalties, interest, and legal consequences. It is essential to ensure accurate reporting, timely filing, and payment of taxes to stay compliant with the tax laws.

ITR returns helps in filing loan application or to raise funds from different sources.

Refund of excess TDS

Excess TDS deductions can be claimed as a refund by filing the ITR when the actual tax liability is lower than the deducted amount.

Avoid Income tax notice

To avoid legal notices, file your ITR on time and accurately as per the criteria defined in the Act.

Visa procurement

Income tax returns are required by certain countries for visa processing & universities may need it to assess eligibility for higher education purposes.

Income evidence

An income tax return is the only document that serves as proof of your current income and its source.

Carry forward of losses

Filing the ITR enables businesses to carry forward losses for up to 8 years, reducing taxable income in the future. Not filing the ITR means missing out on this benefit.